Below are my notes for the book: The Most Important Thing: Uncommon Sense for the Uncommon Investor. I tend to keep notes on things that I have not read in other investment books but if I find that there is an overlap and especially if it was not particularly useful, I will omit that addition into my notes.

Since other investors may be smart, well-informed and highly computerized, you must find an edge they don’t have. You must think of something they haven’t thought of, see things they miss or bring insight they don’t possess. You have to react differently and behave differently. In short, being right may be a necessary condition for investment success, but it won’t be sufficient.

Second-level thinking is deep, complex and convoluted. The second- level thinker takes a great many things into account:

* What is the range of likely future outcomes?

* Which outcome do I think will occur?

* What’s the probability I’m right?

* What does the consensus think?

* How does my expectation differ from the consensus?

* How does the current price for the asset comport with the consensus

view of the future, and with mine?

* Is the consensus psychology that’s incorporated in the price too bullish

or bearish?

* What will happen to the asset’s price if the consensus turns out to be

right, and what if I’m right?

To outperform the average investor, you have to be able to outthink the consensus. Are you capable of doing so? What makes you think so?

Second-level thinkers know that, to achieve superior results, they have to have an edge in either information or analysis, or both. ey are on the alert for instances of misperception.

* Why should a bargain exist despite the presence of thousands of inves- tors who stand ready and willing to bid up the price of anything that’s too cheap?

* If the return appears so generous in proportion to the risk, might you be overlooking some hidden risk?

* Why would the seller of the asset be willing to part with it at a price from which it will give you an excessive return?

* Do you really know more about the asset than the seller does?

* If it’s such a great proposition, why hasn’t someone else snapped it up?

Investing is a popularity contest, and the most dangerous thing is to buy something at the peak of its popularity. At that point, all favorable facts and opinions are already factored into its price, and no new buyers are left to emerge.

The safest and most potentially profitable thing is to buy something when no one likes it. Given time, its popularity, and thus its price, can only go one way: up.

To sum up, I believe that an investment approach based on solid value is the most dependable. In contrast, counting on others to give you a profit regardless of value—relying on a bubble—is probably the least

Like opportunities to make money, the degree of risk present in a market derives from the behavior of the participants, not from securities, strategies and institutions. Regardless of what’s designed into market structures, risk will be low only if investors behave prudently.

I’m firmly convinced that investment risk resides most where it is least perceived, and vice versa:

When everyone believes something is risky , their unwillingness to buy usually reduces its price to the point where it’s not risky at all. Broadly negative opinion can make it the least risky thing, since all optimism has been driven out of its price.

This paradox exists because most investors think quality, as opposed to price, is the determinant of whether something’s risky. But high quality assets can be risky, and low quality assets can be safe. It’s just a matter of the price paid for them. . . . Elevated popular opinion, then, isn’t just the source of low return potential, but also of high risk.

Bottom line: risk control is invisible in good times but still essential, since good times can so easily turn into bad times.

Over a full career, most investors’ results will be determined more by how many losers they have, and how bad they are, than by the greatness of their winners. Skillful risk control is the mark of the superior investor.

Many people possess the intellect needed to analyze data, but far fewer are able to look more deeply into things and withstand the powerful influence of psychology. To say this another way, many people will reach similar cognitive conclusions from their analysis, but what they do with those conclusions varies all over the lot because psychology influences them differently. The biggest investing errors come not from factors that are informational or analytical, but from those that are psychological.

Time and time again, the combination of pressure to conform and the desire to get rich causes people to drop their independence and skepti- cism, overcome their innate risk aversion and believe things that don’t make sense. It happens so regularly that there must be something dependable at work, not a random influence.

The fifth psychological influence is envy. However negative the force of greed might be, always spurring people to strive for more and more, the impact is even stronger when they compare themselves to others. This is one of the most harmful aspects of what we call human nature.

There are two primary elements in superior investing:

• seeing some quality that others don’t see or appreciate (and that isn’t re ected in the price), and

• having it turn out to be true (or at least accepted by the market).

It should be clear from the first element that the process has to begin with investors who are unusually perceptive, unconventional, iconoclastic or early. That’s why successful investors are said to spend a lot of their time being lonely.

skepticism and pessimism aren’t synonymous. Skepticism calls for pessimism when optimism is excessive. But it also calls for optimism when pessimism is excessive.

That’s why the concept of intrinsic value is so important. If we hold a view of value that enables us to buy when everyone else is selling— and if our view turns out to be right—that’s the route to the greatest rewards earned with the least risk.

Since the efficient-market process of setting fair prices requires the involvement of people who are analytical and objective, bargains usually are based on irrationality or incomplete understanding. us, bargains are o en created when investors either fail to consider an asset fairly, or fail to look beneath the surface to understand it thoroughly, or fail to overcome some non-value-based tradition, bias or stricture.

To boil it all down to just one sentence, I’d say the necessary condition for the existence of bargains is that perception has to be considerably worse than reality. at means the best opportunities are usually found among things most others won’t do.

But one of the things I want to do in this chapter is to point out that there aren’t always great things to do, and sometimes we maximize our contribution by being discerning and relatively inactive. Patient opportunism—waiting for bargains—is o en your best strategy.

So here’s a tip: You’ll do better if you wait for investments to come to you rather than go chasing a er them. You tend to get better buys if you select from the list of things sellers are motivated to sell rather than start with a notion as to what you want to own.

The key during a crisis is to be (a) insulated from the forces that require selling and (b) positioned to be a buyer instead. To satisfy those criteria, an investor needs the following things: staunch reliance on value, little or no use of leverage, long-term capital and a strong stomach.

Investors who feel they know what the future holds will act assertively: making directional bets, concentrating positions, levering holdings and count- ing on future growth—in other words, doing things that in the absence of foreknowledge would increase risk. On the other hand, those who feel they don’t know what the future holds will act quite differently: diversifying, hedging, levering less (or not at all), emphasizing value today over growth tomorrow, staying high in the capital structure, and generally girding for a variety of possible outcomes.

Since the investors of the “I know” school, described in chapter 14, feel it’s possible to know the future, they decide what it will look like, build portfolios designed to maximize returns under that one scenario, and largely disregard the other possibilities. The suboptimizers of the “I don’t know” school, on the other hand, put their emphasis on constructing portfolios that will do well in the scenarios they consider likely and not too poorly in the rest.

* We have to practice defensive investing, since many of the outcomes are likely to go against us. It’s more important to ensure survival under negative outcomes than it is to guarantee maximum returns under favorable ones.

* To improve our chances of success, we have to emphasize acting contrary to the herd when it’s at extremes, being aggressive when the mar- ket is low and cautious when it’s high.

His views on market efficiency and the high cost of trading led him to conclude that the pursuit of winners in the mainstream stock markets is unlikely to pay off for the investor. Instead, you should try to avoid hitting losers. I found this view of investing absolutely compelling.

The choice between offense and defense investing should be based on how much the investor believes is within his or her control. In my view, investing entails a lot that isn’t.

I don’t think many investment managers’ careers end because they fail to hit home runs. Rather, they end up out of the game because they strike out too o en—not because they don’t have enough winners, but because they have too many losers. And yet, lots of managers keep swinging for the fences.

Thus, it’s important to return to Bruce Newberg’s pithy observation about the big difference between probability and outcome. Things that aren’t supposed to happen do happen. Short-run outcomes can diverge from the long-run probabilities, and occurrences can cluster.

One way to improve investment results—which we try hard to apply at Oaktree—is to think about what “today’s mistake” might be and try to avoid it.

Most investors think diversification consists of holding many different things; few understand that diversification is effective only if portfolio holdings can be counted on to respond differently to a given development in the environment.

Only investors with unusual insight can regularly divine the probability distribution that governs future events and sense when the potential re- turns compensate for the risks that lurk in the distribution’s negative left- hand tail.

The following are notes from the book: The Intelligent Investor by Ben Graham. Graham was a professor at Columbia, who set forth and popularized the idea of “value investing”. Value investing is about determining the intrinsic value of an investment and buying when the price is markedly below the actual value that investment. The primary factor for profit does not come from the actual growth or success of the investment but from identifying when the actual purchase is mispriced. This is akin to buying items cheaply from a garage sale and selling it for much higher prices on e-bay. Unlike growth investing, which depends on the company growing far beyond what is currently expected or momentum investing which has to do with getting timing right on the market, Graham explains his investment style along the lines of methodical reasoning and sobering calculations.

Notes from The Intelligent Investor:

-To enjoy a reasonable chance for continued better than average results, the investor must follow policies which are (1) inherently sound and promising, and (2) not popular on Wall Street.

-don’t lose money. Its harder to make the money back once you’ve lost money.

Investing, according to Graham, consists equally of three elements:

• you must thoroughly analyze a company, and the soundness of its underlying businesses, before you buy its stock;

• you must deliberately protect yourself against serious losses;

• you must aspire to “adequate,” not extraordinary, performance.

-two inflation fighters: REITs and TIPS (TIPS paper gain is taxable income, better in tax-exempt account)

-the intelligent investor must never forecast the future exclusively by extrapolating the past.

-The value of any investment is, and always must be, a function of the price you pay for it.

-the corollary to that law of financial history is that the markets will most brutally surprise the very people who are most certain that their views about the future are right.

-By the rule of opposites,” the more enthusiastic investors become about the stock market in the long run, the more certain they are to be proved wrong in the short run.

-technical trading would not merit buying a stock when it falls but if the value of the investment is assured when you buy it, then buying when a stock drops would make sense. Otherwise, if youre in a pure technical trading environment such as crypto, you’re better off following those principles

In these cases the market has sufficient skepticism as to the continuation of the unusually high profits to value them con- servatively, and conversely when earnings are low or nonexistent. (Note that, by the arithmetic, if a company earns “next to nothing”

The better the quality of a common stock, the more speculative it is likely to be

investing isn’t about beating oth- ers at their game. It’s about controlling yourself at your own game.

In our own experience we have noted among them (financial analysts) a pervasive attitude which we think tends to impair what could otherwise be more useful advisory work. This is their general view that a stock should be bought if the near-term prospects of the business are favorable and should be sold if these are unfavorable—regardless of the current price.

We suggest that analysts work out first what we call the “past-performance value,” which is based solely on the past record. This would indicate what the stock would be worth. The second part of the analysis should consider to what extent the value based solely on past performance should be modified because of new conditions expected in the future.

Which factors determine how much you should be willing to pay for a stock? What makes one company worth 10 times earnings and another worth 20 times? How can you be reasonably sure that you are not overpaying for an apparently rosy future that turns out to be a murky nightmare?

Graham feels that five elements are decisive.1 He summarizes them as:

• the company’s “general long-term prospects”

• the quality of its management

• its financial strength and capital structure

• its dividend record

• and its current dividend rate.

Let’s look at these factors in the light of today’s market.

The long-term prospects. Nowadays, the intelligent investor should begin by downloading at least five years’ worth of annual reports (Form 10-K) from the company’s website. Get one year of quarterly reports too

Then comb through the financial state- ments, gathering evidence to help you answer two overriding ques- tions. What makes this company grow? Where do (and where will) its profits come from? Among the problems to watch for:

• The company is a “serial acquirer.” An average of more than two or three acquisitions a year is a sign of potential trouble. After all, if the company itself would rather buy the stock of other busi- nesses than invest in its own, shouldn’t you take the hint and look elsewhere too? And check the company’s track record as an acquirer. Watch out for corporate bulimics—firms that wolf down big acquisitions, only to end up vomiting them back out. Lucent, Mattel, Quaker Oats, and Tyco International are among the com- panies that have had to disgorge acquisitions at sickening losses. Other firms take chronic write-offs, or accounting charges proving that they overpaid for their past acquisitions. That’s a bad omen for future deal making.

• The company is an OPM addict, borrowing debt or selling stock to raise boatloads of Other People’s Money. These fat infusions of OPM are labeled “cash from financing activities” on the statement of cash flows in the annual report. They can make a sick company appear to be growing even if its underlying businesses are not generating enough cash—as Global Crossing and WorldCom showed not long ago.

you study the sources of growth and profit, stay on the lookout for positives as well as negatives. Among the good signs:

• The company has a wide “moat,” or competitive advantage. Like castles, some companies can easily be stormed by marauding competitors, while others are almost impregnable. Several forces can widen a company’s moat: a strong brand identity (think of Harley Davidson, whose buyers tattoo the company’s logo onto their bodies); a monopoly or near-monopoly on the market; economies of scale, or the ability to supply huge amounts of goods or services cheaply (consider Gillette, which churns out razor blades by the billion); a unique intangible asset (think of Coca- Cola, whose secret formula for flavored syrup has no real physical value but maintains a priceless hold on consumers); a resistance to substitution (most businesses have no alternative to electricity, so utility companies are unlikely to be supplanted any time soon).5

The company is a marathoner, not a sprinter. By looking back at the income statements, you can see whether revenues and net earnings have grown smoothly and steadily over the previous 10 years. A recent article in the Financial Analysts Journal confirmed what other studies (and the sad experience of many investors) have shown: that the fastest-growing companies tend to overheat and flame out.6 If earnings are growing at a long-term rate of 10% pretax (or 6% to 7% after-tax), that may be sustainable. But the 15% growth hurdle that many companies set for themselves is delusional. And an even higher rate—or a sudden burst of growth in one or two years—is all but certain to fade, just like an inexperi- enced marathoner who tries to run the whole race as if it were a 100-meter dash.

• The company sows and reaps. No matter how good its products or how powerful its brands, a company must spend some money to develop new business. While research and development spending is not a source of growth today, it may well be tomor- row—particularly if a firm has a proven record of rejuvenating its businesses with new ideas and equipment. The average budget for research and development varies across industries and com- panies. In 2002, Procter & Gamble spent about 4% of its net sales on R & D, while 3M spent 6.5% and Johnson & Johnson 10.9%. In the long run, a company that spends nothing on R & D is at least as vulnerable as one that spends too much.

The quality and conduct of management. A company’s execu- tives should say what they will do, then do what they said. Read the past annual reports to see what forecasts the managers made and if they fulfilled them or fell short. Managers should forthrightly admit their failures and take responsibility for them, rather than blaming all-purpose scapegoats like “the economy,” “uncertainty,” or “weak demand.” Check whether the tone and substance of the chairman’s letter stay constant, or fluctuate with the latest fads on Wall Street. (Pay special attention to boom years like 1999: Did the executives of a cement or underwear company suddenly declare that they were “on the leading edge of the transformative software revolution

To fine-tune the definition of owner earnings, you should also subtract from reported net income:

•any costs of granting stock options, which divert earnings away from existing shareholders into the hands of new inside owners

-any “unusual,” “nonrecurring,” or “extraordinary” charges

-any “income” from the company’s pension fund.

Next, look at the company’s capital structure. Turn to the balance sheet to see how much debt (including preferred stock) the company has; in general, long-term debt should be under 50% of total capital. In the footnotes to the financial statements, determine whether the long-term debt is fixed-rate (with constant interest payments) or vari- able (with payments that fluctuate, which could become costly if inter- est rates rise).

In our opinion, the proper mode of calculation would be first to consider the indicated earning power on the basis of full income- tax liability, and to derive some broad idea of the stock’s value based on that estimate. To this should be added some bonus figure, representing the value per share of the important but temporary tax exemption the company will enjoy. (Allowance must be made, also, for a possible large-scale dilution in this case.

In short, pro forma earnings enable companies to show how well they might have done if they hadn’t done as badly as they did.2 As an intelligent investor, the only thing you should do with pro forma earn- ings is ignore them.

A few pointers will help you avoid buying a stock that turns out to be an accounting time bomb:

Read backwards. When you research a company’s financial reports, start reading on the last page and slowly work your way toward the front. Anything that the company doesn’t want you to find is buried in the back—which is precisely why you should look there first.

Read the notes. Never buy a stock without reading the footnotes to the financial statements in the annual report. Usually labeled “sum- mary of significant accounting policies,” one key note describes how the company recognizes revenue, records inventories, treats install- ment or contract sales, expenses its marketing costs, and accounts for the other major aspects of its business.7 In the other footnotes, watch for disclosures about debt, stock options, loans to customers, reserves against losses, and other “risk factors” that can take a big chomp out of earnings.

By contrast, those who emphasize protection are always espe- cially concerned with the price of the issue at the time of study. Their main effort is to assure themselves of a substantial margin of indicated present value above the market price—which margin could absorb unfavorable developments in the future.

Keeping your money spread across many stocks and industries is the only reliable insurance against the risk of being wrong.

But if it is true that a fairly large segment of the stock mar- ket is often discriminated against or entirely neglected in the stan- dard analytical selections, then the intelligent investor may be in a position to profit from the resultant undervaluations.

But to do so he must follow specific methods that are not gener- ally accepted on Wall Street, since those that are so accepted do not seem to produce the results everyone would like to achieve. It would be rather strange if—with all the brains at work profession- ally in the stock market—there could be approaches which are both sound and relatively unpopular. Yet our own career and reputation have been based on this unlikely fact.

Mason Value Trust like to see rising returns on invested capital, or ROIC—a way of measuring how efficiently a company generates what Warren Buffett has called “owner earnings.”

Finally, most leading professional investors want to see that a com- pany is run by people who, in the words of Oakmark’s William Nygren, “think like owners, not just managers.” Two simple tests: Are the company’s financial statements easily understandable, or are they full of obfuscation? Are “nonrecurring” or “extraordinary” or “unusual” charges just that, or do they have a nasty habit of recurring?

Longleaf’s Mason Hawkins looks for corporate managers who are “good partners”—meaning that they communicate candidly about problems, have clear plans for allocating current and future cash flow, and own sizable stakes in the company’s stock (preferably through cash purchases rather than through grants of options). But “if man- agements talk more about the stock price than about the business,” warns Robert Torray of the Torray Fund, “we’re not interested.” Christopher Davis of the Davis Funds favors firms that limit issuance of stock options to roughly 3% of shares outstanding.

Robert Rodriguez of FPA Capital Fund turns to the back page of the company’s annual report, where the heads of its operating divi- sions are listed. If there’s a lot of turnover in those names in the first one or two years of a new CEO’s regime, that’s probably a good sign; he’s cleaning out the dead wood. But if high turnover continues, the turnaround has probably devolved into turmoil.

No matter which techniques they use in picking stocks, successful investing professionals have two things in common: First, they are dis- ciplined and consistent, refusing to change their approach even when it is unfashionable. Second, they think a great deal about what they do and how to do it, but they pay very little attention to what the market is doing.

Observation over many years has taught us that the chief losses to investors come from the purchase of low-quality securities at times of favorable business conditions. The purchasers view the current good earnings as equivalent to “earning power” and assume that prosperity is synonymous with safety. It is in those years that bonds and preferred stocks of infe- rior grade can be sold to the public at a price around par, because they carry a little higher income return or a deceptively attractive conversion privilege. It is then, also, that common stocks of obscure companies can be floated at prices far above the tangible investment, on the strength of two or three years of excellent growth.

In investment theory there is no reason why carefully estimated future earnings should be a less reliable guide than the bare record of the past; in fact, security analysis is coming more and more to prefer a competently executed evaluation of the future. Thus the growth-stock approach may supply as dependable a margin of safety as is found in the ordinary investment— provided the calculation of the future is conservatively made, and provided it shows a satisfactory margin in relation to the price paid.

Graham is saying that there is no such thing as a good or bad stock; there are only cheap stocks and expensive stocks. Even the best company becomes a “sell” when its stock price goes too high, while the worst com- pany is worth buying if its stock goes low enough

For the enterprising investor this means that his operations for profit should be based not on optimism but on arithmetic. For every investor it means that when he limits his return to a small figure—as formerly, at least, in a conventional bond or preferred stock—he must demand convincing evidence that he is not risking a substantial part of his principal.

Have the courage of your knowledge and experience. If you have formed a conclusion from the facts and if you know your judgment is sound, act on it— even though others may hesitate or differ.” (You are neither right nor wrong because the crowd disagrees with you. You are right because your data and reasoning are right.) Similarly, in the world of securities, courage becomes the supreme virtue after adequate knowledge and a tested judgment are at hand.

Imagine that you find a stock that you think can grow at 10% a year even if the market only grows 5% annually. Unfortunately, you are so enthusiastic that you pay too high a price, and the stock loses 50% of its value the first year. Even if the stock then generates double the market’s return, it will take you more than 16 years to overtake the market—simply because you paid too much, and lost too much, at the outset.

The Nobel-prize–winning psychologist Daniel Kahneman explains two factors that characterize good decisions:

• “well-calibrated confidence” (do I understand this investment as well as I think I do?)

• “correctly-anticipated regret” (how will I react if my analysis turns out to be wrong?).

Before you invest, you must ensure that you have realistically assessed your probability of being right and how you will react to the consequences of being wrong.

This post lists my notes from reading the classic investment book: Common Stocks & Uncommon Profits. Written by the famous investment manager – Philip Fisher, the book espouses a growth investment philosophy. Growth investing involves identifying companies that will accelerate its overall market cap and net income much farther than is expected against current market expectations. The focus is not on identifying companies that are doing decently now but on companies that will be phenomenal in the future and would only require that you hold it through the journey.

The notes are split into the 15-point list that describes the attributes he’s identified for any well-run company and the second part are general comments that I found useful throughout the book.

1. Does the company have products or services with sufficient market potential to make possible a sizable increase in sales for at least several years?

2. Does the management have a determination to continue to develop products or processes that will still further increase total sales potentials when the growth potentials of currently attractive product lines have largely been exploited

3.How effective are the company’s research and development efforts in relation to its size?

4. Does the company have an above-average sales organization?

5. Does the company have a worthwhile profit margin?

6. What is the company doing to maintain or improve profit margins?

7. Does the company have outstanding labor and personnel relations?

8. Does the company have outstanding executive relations?

9. Does the company have depth to its management?

10. How good are the company’s cost analysis and accounting controls?

11. Are there other aspects of the business, somewhat peculiar to the industry involved, which will give the investor important clues as to how outstanding the company may be in relation to its competition?

12. Does the company have a short-range or long-range outlook in regard to profits?

13. In the foreseeable future will the growth of the company require sufficient equity financing so that the larger number of shares then outstanding will largely cancel the existing stockholders’ benefit from this anticipated growth?

14. Does the management talk freely to investors about its affairs when things are going well but “clam up” when troubles and disappointments occur?

15. Does the company have a management of unquestionable integrity?

General Notes

Scuttlebutt means avoiding malarkey mills and seeking information from competitors, customers, and suppliers, all of whom have a vested interest in the target company, and few of whom have any reason to see the firm unrealistically.

Such a study indicates that the greatest investment reward comes to those who by good luck or good sense find the occasional company that over the years can grow in sales and profits far more than industry as a whole.

Go to five companies in an industry, ask each of them intelligent questions about the points of strength and weakness of the other four, and nine times out of ten a surprisingly detailed and accurate picture of all five will emerge.

It is equally astonishing how much can be learned from both vendors and customers about the real nature of the people with whom they deal. Research scientists in universities, in government, and in competitive companies are another fertile source of worthwhile data. So are executives of trade associations.

The investor usually obtains the best results in companies whose engineering or research is to a considerable extent devoted to products having some business relationship to those already within the scope of company activities.

Does the company now recognize that in time it will almost certainly have grown up to the potential of its pres- ent market and that to continue to grow it may have to develop further new markets at some future time?

[R&D] Figures of this sort can prove a crude yardstick that may give a worthwhile hint that one company is doing an abnormal amount of research or another not nearly enough. But unless a great deal of further knowledge is obtained, such figures can be misleading. One reason for this is that companies vary enormously in what they include or exclude as research and development expense.

A simpler and often worthwhile method is to make a close study of how much in dollar sales or net profits has been con- tributed to a company by the results of its research organization during a particular span, such as the prior ten years. An organization which inrelation to the size of its activities has produced a good flow of prof- itable new products during such a period will probably be equally pro- ductive in the future as long as it continues to operate under the same general methods.

Yet, strange as it seems, the relative efficiency of a company’s sales, advertising, and distributive organizations receives far less attention from most investors, even the careful ones, than do pro- duction, research, finance, or other major subdivisions of corporate activity

However, outstanding production, sales, and research may be considered the three main columns upon which such success is based.

If workers feel that they are fairly treated by their employer, a background has been laid wherein efficient leadership can accomplish much in increasing productivity per worker. Furthermore, there is always considerable cost in training each new worker.Those companies with an abnormal labor turnover have therefore an element of unnecessary expense avoided by better-managed enterprises.

Companies with good labor relations usually are ones making every effort to settle grievances quickly.

the investor should be sensitive to the attitude of top management toward the rank-and-file employees. Underneath all the fine-sounding generalities, some managements have little feeling of responsibility for, or interest in, their ordinary workers.

The company offering greatest investment opportunities will be one in which there is a good executive climate. Executives will have confidence in their president and/or board chairman. This means, among other things, that from the lowest levels on up there is a feeling that promotions are based on ability, not factionalism

As has been true many times before and since, it is the constant leadership in engineering, not patents, that is the fundamental source of protection. The investor must be at least as careful not to place too much importance on patent protection as to recognize its significance in those occasional places where it is a major factor in appraising the attractiveness of a desirable investment.

In any event, the investor will do well to exclude from investment any company that withholds or tries to hide bad news.

There is only one real protection against abuses like these.This is to confine investments to companies the managements of which have a highly developed sense of trusteeship and moral responsibility to their stockholders.

Regardless of how high the rating may be in all other matters, however, if there is a serious question of the lack of a strong management sense of trusteeship for stockholders, the investor should never seriously consider participating in such an enterprise.

The successful investor is usually an individual who is inherently interested in business problems. This results in his discussing such matters in a way that will arouse the interest of those from whom he is seeking data

I believe there are three reasons, and three reasons only, for the sale of any common stock which has been originally selected according to the investment principles already discussed.The first of these reasons should be obvious to anyone. This is when a mistake has been made in the original purchase and it becomes increasingly clear that the fac- tual background of the particular company is, by a significant margin, less favorable than originally believed

More money has probably been lost by investors holding a stock they really did not want until they could “at least come out even” than from any other single reason.

Sales should always be made of the stock of a company which, because of changes resulting from the pas- sage of time, no longer qualifies in regard to the fifteen points outlined in Chapter Three to about the same degree it qualified at the time of purchase. This is why investors should be constantly on their guard. It explains why it is of such importance to keep at all times in close contact with the affairs of companies whose shares are held.

When companies deteriorate in this way they usually do so for one of two reasons. Either there has been a deterioration of management, or the company no longer has the prospect of increasing the markets for its product in the way it formerly did.

There is a good test as to whether companies no longer adequately qualify in regard to this matter of expected further growth.This is for the investor to ask himself whether at the next peak of a business cycle, regardless of what may happen in the meantime, the comparative per- share earnings (after allowances for stock dividends and stock splits but not for new shares issued for additional capital) will probably show at least as great an increase from present levels as the present levels show from the last known peak of general business activity. If the answer is in the affirmative, the stock probably should be held. If in the negative, it should probably be sold.

If the growth rate is so good that in another ten years the company might well have quadrupled, is it really of such great concern whether at the moment the stock might or might not be 35 per cent overpriced? That which really matters is not to disturb a position that is going to be worth a great deal more later.

What is most important, however, is that stocks are not bought in companies where the dividend pay-out is so emphasized that it restricts realizable growth.

It never seems to occur to them, much less to their advisors, that buying a company without having sufficient knowledge of it may be even more dangerous than having inadequate diversification.

By giving heavy emphasis to the “stock that hasn’t gone up yet” they are unconsciously subscribing to the delusion that all stocks go up about the same amount and that the one that has already risen a lot will not climb further, while the one that has not yet gone up has something “due” it

To be a truly conservative investment a company—for a majority if not for all of its product lines—must be the lowest-cost producer or about as low a cost producer as any competitor. It must also give promise of continuing to be so in the future.

In the competitive world of commerce it is vital to make the potential customer aware of the advantages of a product or service.This awareness can be created only by understanding what the potential buyer really wants (sometimes when the customer himself doesn’t clearly recognize why these advantages appeal to him) and explaining it to him not in the seller’s terms but in his terms.

A conservative firm will have outstanding research and technical effort. A balance between cost-efficient operation and allowing for ingenuity

Companies with above-average financial talent have several significant advantages. Knowing accurately how much they make on each product, they can make their greatest efforts where these will produce maximum gains. Intimate knowledge of the extent of each element of costs, not just in manufacturing but in selling and research as well, spotlights in even minor phases of company activity the places where it is logical to make special efforts to reduce costs, either through technological innovations or by improving people’s specific assignments.

In a world where change is occurring at an ever-increasing pace, it is (1) a company capable of developing a flow of new and profitable products or product lines that will more than balance older lines that may become obsolete by the technological innovations of others; (2) a company able now and in the future to make these lines at costs sufficiently low so as to generate a profit stream that will grow at least as fast as sales and that even in the worst years of general business will not diminish to a point that threatens the safety of an investment in the business; and (3) a company able to sell its newer products and those which it may develop in the future at least as profitably as those with which it is involved today.

[Edward Heller] He said that behind every unusually successful corporation was this kind of determined entrepreneurial personality with the drive, the original ideas, and the skill to make such a company a truly worthwhile investment.

The force that causes such things to happen, that creates one company in an industry that is an outstanding investment vehicle and another that is average, mediocre, or worse, is essentially people.

In general, however, the company with real investment merit is the company that usually promotes from within.This is because all compa- nies of the highest investment order (these do not necessarily have to be the biggest and best-known companies) have developed a set of policies and ways of doing things peculiar to their own needs. If these special ways are truly worthwhile, it is always difficult and frequently impossi- ble to retrain those long accustomed to them to different ways of get- ting things done.The higher up in an organization the newcomer may be, the more costly the indoctrination can be.

A worthwhile clue is available to all investors as to whether a management is predominantly one man or a smoothly working team (this clue throws no light, however, on how good that team may be).The annual salaries of top management of all publicly owned companies are made public in the proxy statements. If the salary of the number-one man is very much larger than that of the next two or three, a warning flag is fly- ing. If the compensation scale goes down rather gradually, it isn’t.

However much policies may differ among companies, there are three elements that must always be present if a company’s shares are to be worthy of holding for conservative, long-range investment.

1. The company must recognize that the world in which it is operating is changing at an ever-increasing rate.

2. There must always be a conscious and continuous effort, based on fact, not propaganda, to have employees at every level, from the most newly hired blue-collar or white-collar worker to the highest levels of management, feel that their company is a good place to work.

3.Management must be willing to submit itself to the disciplines required for sound growth.

In all countries the morale effects appear striking when worker teams not only report directly to top management levels but also know their reports will be heeded and their accomplishments recognized and acknowledged.

Meanwhile, companies that do perfect advantageous people-oriented policies and techniques usually find more and more ways to benefit from them. For these companies, such policies and techniques—these special ways of approaching problems and of solving them—are in a sense proprietary.

Profitability can be expressed in two ways. The fundamental way, which is the yardstick used by most managements, is the return on invested assets.This is the factor that will cause a company to decide whether to go ahead with a new product or process. What percent return can the company expect on the part of its capital invested in this particular way in comparison to what the return might be if the same amount of its assets was employed in some other way? It is considerably more difficult for the investor to use this yardstick than it is for the corporate executive.What the investor usually sees is not the return on a specific amount of present-day dollars utilized in a specific subdivision of the business but the total earnings of the business as a percentage of its total assets.When the cost of capital equipment has risen as much as it has in the last forty years, comparisons of the return on total invested capital between one company and another may be so distorted by variations in the price levels at which different companies made major expenditures that the figures are highly misleading. For this reason, comparing the profit margins per dollar of sales may be more helpful as long as one other point is kept in mind.This is that a company that has a high rate of sales in relation to assets may be a more profitable company than one with a higher profit margin to sales but a slower rate of sales turnover.

However, while from the standpoint of profitability return on investment must be considered as well as profit margin on sales, from the standpoint of safety of investment all the emphasis is on profit margin on sales.

Now let us turn from this background discussion of relative profitability to the heart of the third dimension of conservative investing— namely, the specific characteristics that enable certain well-managed companies to maintain above-average profit margins more or less indefinitely. Possibly the most common characteristic is what businessmen call the“economies of scale.”

On the other hand, when a company clearly becomes the leader in its field, not just in dollar volume but in profitability, it seldom gets dis- placed from this position as long as its management remains highly competent.

What enables a company to obtain this advantage of scale in the first place? Usually getting there first with a new product or service that meets worthwhile demand and backing this up with good enough marketing, servicing, product improvement, and, at times, advertising to keep existing customers happy and coming back for more. This frequently establishes an atmosphere in which new customers will turn to the leader largely because that leader has established such a reputation for performance (or sound value) that no one is likely to criticize the buyer adversely for making this particular selection.

Another which we believe is of particular interest is the difficulty of competing with a highly successful, established producer in a technological area where the technology depends on not one scientific discipline but the interplay of two or preferably several quite different disciplines. I believe that some of these multidisciplinary technological companies, in not all of which is electronics a significant factor, have recently proven some of the finest opportunities for truly farsighted investing.

An example is a company that has created in its customers the habit of almost automatically specifying its products for reorder in a way that makes it rather uneconomical for a competitor to attempt to displace them.Two sets of conditions are necessary for this to happen. First, the company must build up a reputation for quality and reliability in a product (a) that the customer recognizes is very important for the proper conduct of his activities, (b) where an inferior or malfunctioning product would cause serious problems, (c) where no competitor is serving more than a minor segment of the market so that the dominant company is nearly synonymous in the public mind with the source of supply, and yet (d) the cost of the product is only a quite small part of the customer’s total cost of operations. Second, it must have a product sold to many small customers rather than a few large ones. These customers must be sufficiently specialized in their nature that it would be unlikely for a potential competitor to feel they could be reached through advertising media such as magazines or television.They constitute a market in which, as long as the dominant company maintains the quality of its product and the adequacy of its service, it can be displaced only by informed salesmen making individual calls.

The conservative investor must be aware of the nature of the current financial-community appraisal of any industry which he is interested

For a company to be a truly worthwhile investment, it must not only be able to sell its products, but also be able to appraise changing needs and desires of its customers; in other words, to master all that is implied in a true concept of marketing

I began realizing that, all the then current wall street opinion to the contrary, what really counts in determining whether a stock is cheap or overpriced is not its ratio to its current years earnings but its ratio to the earnings a few years ahead

Hope you found these notes useful. I use ideas like these within my own investment management philosophy.

In the context of investing, leverage means using additional money that’s taken out as a loan to invest into a product that is expected to produce higher returns. If someone takes a bank loan of 4% interest to create a coffee shop that can produce 20% return within the year, they will have made successful use of leverage.

In the context of investing, leverage means using additional money that’s taken out as a loan to invest into a product that is expected to produce higher returns. If someone takes a bank loan of 4% interest to create a coffee shop that can produce 20% return within the year, they will have made successful use of leverage.

There are also other forms of leverage available such as using options and futures within the stock market. By buying these derivatives, an individual can create a stake in a company that amplifies a bet times 100. Someone can purchase a call on Apple (AAPL) stock at $200 and when the price increases by 10%, they can cash in on the call for a sizable profit (representing 100% gain – the cost of the call). The potential to produce substantial returns by the use of derivatives may explain the proliferation of “options or future(fx) traders” out there. It’s a way to get involved in the stock market with relatively low sums of money and potentially produce significant income. While the potential for higher income is available, there are multiple risks that become present once you introduce derivatives into your investment portfolio.

1. Derivatives amplify your potential for profit…and loss.

Sure, you can make a lot more money with derivatives but you now also have the potential to lose a lot more money. If you’re wrong on a specific bet, then you could end up with a derivative that is worthless. The potential for your portfolio to go to 0 becomes much more steeper. Even if you are using derivatives in a way that is meant to lower the risk of short-term volatility, you pay extra for that type of insurance. If you end up being wrong even 3-5 times in a row, which can be very easy to do, you may find out that your entire portfolio gets wiped out.

2. Once you take a major loss, your psychology will highly encourage you to continue…much like that of a gambler.

Assuming at some point you do lose a major portion of your money by taking a higher risk bet on a derivative, that type of loss will incentivize you to take even riskier bets. Once your portfolio is down 40%, you would need to make 66% on your money to hit break-even point again. With a need to hit break-even again, you’d realize that the fastest way to get back there again is an even bigger risk. This type of psychological reasoning keeps you in the game until you have no chips left to play.

3. Once you take a major gain, your psychology will be influenced to take risky decisions as well.

Let’s assume you gain 40% or even 100% within a very short time period. The risk and bet you have taken will prop up your psychology to become more confident and take even bigger risks, as you might reason that it will continue to be that easy. After increasing your money by however much, you may find that you get attached to that larger number. Then, assuming you lose a good sum on a wrong bet (which would be inevitable the longer you are “playing the stock market”), you become incentivized to play out the psychological dynamics discussed in #2.

4. Derivatives can expire over time ranging from a few days to years, introducing a market timing element to the investing.

Because there is an expiration date on the derivative, you not only have to be right but you need to be right about when it will happen. The timing aspect of derivatives can cause a rushed feeling within your psychology, causing you to take bets that backfire inappropriately. Time works against you when it comes to derivatives, which is unlike buying and holding securities for the long-term (longer holding periods is associated with increased returns).

Thus, there are many potential dangers to using derivatives in investing. For a long-term investor who desires to increase their earnings without the influence of nefarious psychological tendencies, a simple buy and hold approach would suffice.

Recently, there has been a strong push within the investment community towards passive diversification of investments through the use of ETFs and index funds. With programs that offer incredibly low cost-basis fees, down to even 0 fees, it can seem quite enticing to own such broadly diversified securities.

The rationale behind general passive investing (through ETFs and index funds) is predicated on two factors. The first factor being that individuals will not be able to beat the stock market as a whole as it is highly efficient (aka efficient market hypothesis), where the securities themselves reflect true intrinsic value at any given moment. The second factor is that the economy as a whole will continue an upwards trend over the long-term, as innovation within a capitalist society will spark general prosperity. Given these two factors, we have emerged with a general consensus that leaving a bulk of your net worth within a broad-based investment fund such as the SP500, a target date index fund or a robo-advisor is a generally safe option. While it is true that the economy as a whole is mostly efficient with processing recent information into the price of a security, there are unspoken downsides with a traditional passive investment strategy.

Here are the downsides of traditional diversification through passive investment strategies:

1. Through the use of broad-based passive investments, your portfolio will be highly correlated with the general outlook of the stock market at all given times. While this protects you from the downside of being a poor “individual stock-picker”, your portfolio will also have a slim chance of being able to beat the market on a consistent basis. There are a number of quantitative strategies proposing to beat the market through analysis of macroeconomic factors or past data of volatility within various classes of securities. These types of predictions amount to shaky guesses at best. If someone was able to consistently “guess” the market’s direction in the short-term on a repeatable basis, they would be trillionaires. It is also equally suspicious to assume the next 10 years of a certain asset class will be similar to the last 10 years.

If we were to look at who is able to consistently beat the market over the long-term, we would find that it is not the “top-down” macro people who are consistently beating the market over the long-term. The people beating the markets consistently are often completing “bottom-up” fundamental analysis of individual securities. This makes sense because it’s much easier to figure out how an individual security will do over a long-term period than it is to figure out the entire direction of an economy over the short-term on a repeated basis. Basically, using ETFs and index funds, even if you have “specialized” strategies, makes it very difficult to beat the market, not factoring in the luck of educated macro guesses. The lesson here: broad diversification through ETFs and index funds is very likely to lead you to average results and prevent you from being able to achieve consistently better investment returns. If you’re fine with average results (and most people should be as it is difficult to beat the market), this should not be a problem. But for those with the ability to identify securities that will provide larger gains, or an ability to identify individuals who are capable of doing so, the average path would not be a reasonable option.

2. Because a traditional passive investment strategy is exclusively focused on the “long-term”, it is often rationalized that an individual could dump their entire excess cash into the stock market at any point and forget about it. However, if you were to dump your excess cash into the stock market at the peak of 2007 for example, you would find that you would have broken even by 2017/2018, after over a decade. While it is arguably true that over a long-term period of 30-50 years, this would be irrelevant but why lose out when this could have been avoided? This is the rationale that many investors ironically take when looking at these long-term investment strategies.

When resigning to a broad-based passive investing philosophy that invests in the market as a whole, the investor has a negative incentive to focus on the short-term and try market timing because their investments are recognizably subject to short-term macroeconomic factors. This incentive explains why many people are proposing in 2018 to put less money overall into investments because they are worried about a market crash. Overall, this reasoning is limiting because there could be good deals out there for individual securities that would not be as susceptible to market crashes, and would offer opportunities for stable dividends and future potential growth. Being able to identify individual securities that are already cheap would remove a need to try market timing. The other limiting factor is that the market as a whole may continue to keep increasing for a few more years despite all the predictions. Look at how many people were able to predict the Great Recession in 2008, has anything changed with our forecasting abilities since then?

While a lot of this writing was spent criticizing modern diversification strategies, it remains a good option for investors who want to automate the investing process and are truly in it for the long-term. But for those who are particularly susceptible to short-term fluctuations within the stock market or are interested in pursuing better than average market results, they would be better off with strategies such as value investing. This rationale is a large driver for the investing philosophy at Taher Financial Planning.

Warren Buffett is the most distinguished investor in existence today. Often ranking somewhere in the top 4 of the Forbes 100 list through a large ownership stake in the Berkshire Hathaway company, we can assume that he knows a thing or two about business. Within the book “The Essays of Warren Buffett: Lessons For Corporate America“, we receive a first-hand account of the way Warren Buffett perceives the responsibilities of corporate management. Buffett presents as a remarkably lucid investor and businessman. He frequently offer rational, yet strangely simple insights into how a business should be run. Below are the most interesting arguments I have found within the book:

#1: Management’s first priority is to the company’s shareholders.

The actual owners of the company are the shareholders. Management is entrusted to execute business plans that create more value by the owners. If management is recklessly wasting resources, they are a detriment to the company. Management should be held accountable for achieving business results. If they are unable to effectively operate with the hand they’re dealt, they should be removed. The best companies to invest in, are the ones with managers who have this priority in mind.

#2: Franchise value is what really counts.

While achieving business results are important, they should not come at the cost of franchise value. For example, you can raise the prices of your product or service by 20% this year and enjoy momentarily increased profits. It will look good on paper but by doing so, you could harm your brand’s value and destroy good relations you may have with any of your customer base. Some people might leave and never come back. They might tell their friends and family not to associate with your business. It’s a huge mistake to sacrifice your long-term brand to achieve short-term objectives. The reputation of the business is important to maintain.

#3: Bigger doesn’t mean better.

Just because a company has consistently increasing revenues, doesn’t mean that it’s a great company. If the business’s cost structure grows at the same rate that revenues do, then the company itself is never creating true growth. While increased revenues for a company might look good for the managers who can claim they have increased sales by x%, the more holistic look would be to check how operating profits have changed for the better.

If a company has a great business segment that is operating efficiently, management may also deal with a ‘corporate imperative’ to rationalize a dive into a new venture with their net profits. It would be very easy to create a rationale on how a new project will add value to the company but Buffett’s take is that the claims are often larger than the reality. Managers should critically evaluate the extent that new business projects will create true additional value for the company. If there are simple alternatives such as share buybacks or even distributing dividends, these actions would be preferable to speculative, ego-driven projects.

#4: Be discerning of who you associate with.

Having someone who is merely smart on your team is not enough. There are plenty of intelligent people out there. It is much more rare to find an intelligent person who is energetic and ethical. According to Buffett, if someone isn’t ethical, you may as well forget about intelligent or energetic. If you’re going to work with someone, you should make sure their first concern is doing the right thing, otherwise you run the risk of them making poor decisions on your behalf. Finally, life itself is enhanced along with the quality of our business matters when working with people we admire, like and trust.

#5: Focus on business economics, not business accounting.

Many managers become understandably focused with the “bottom-line” results of the work that they complete. Some executives may engage in accounting schemes to cover up their business mishaps.For example, selling a profitable business unit to maintain the image that a company is continually bringing in profits every quarter, even at the cost of long-term potential is a terrible move. Some executives may shy away from decisions that would look poor on paper but great in reality. If a company is losing money and requires more cash to make the appropriate investments into itself, keeping a high dividend rate for historical reasons makes no sense. The real focus should not be on how the business’s numbers would look on paper but on how the business is doing in reality. That type of focus will lead to profitable long-term results.

#6: Master your emotions.

This was a strong lesson implicitly resonating throughout the book. Buffett shows that its not just intelligence that matters for investors and business people but our ability to control emotions is a huge factor in our success. Greed can cause executives to overstate business success rather than showing reality. Fear can cause people to take actions that harms the business brand, employee morale, etc. If we can’t get past the discomfort of going against the crowd, then we can fall into group-think and make the same blunders that other people make. Our ability to think rationally and not let our pride get in the way is of the utmost importance. If we are unable to effectively control our emotions, we are bound for radical errors.

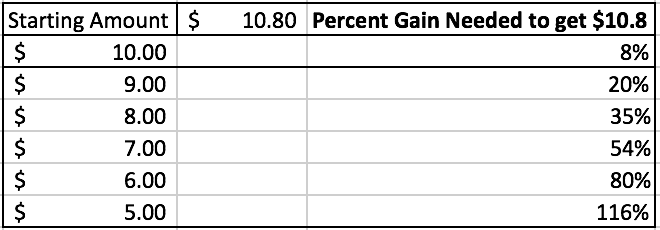

Compound interest is a term that many have heard often but is rarely well understood. The definition on wikipedia is as listed:

Compound interest – is the addition of interest to the principal sum of a loan or deposit, or in other words, interest on interest.

Well, that sounds almost simple – the money you make, will make even more money in the future. But what exactly does that mean in practical terms? This may be where most of the confusion comes in from.

In the above tables, we can see an assumption of different interest rates. These interest rates are tested on the growth of just $1 over different decades. What we’ll find is that the one dollar will grow to about $1.96 to $2.59, about double growth in 10 years for 7-10% interest rates. But by the 20th year, the growth is even higher, ranging from $3.86 – $6.72. The most astounding realization is that by the 40th year the dollar becomes $14.97 – $45.25, a 15 to 45 times return.

In effect, we can learn multiple lessons from this short example:

- For every dollar we spend, we are not just losing only a dollar but we are losing all the future potential growth that the dollar would bring.

- The amount of time that the dollar has to grow will have a huge impact. The difference between a dollar thats been invested for 20 years (at $3.86) and 40 years (at $14.97) is extreme. It’s better by a long-shot to have money to invest as early as possible than getting started later.

- Small differences in interest rate assumptions can have a huge impact. Meaning if you are being charged large fees such as the financial industry’s normal of 1%, it can have a huge effect on your long-term gains. Thus, it is important that you assess whether there is a true premium of investment return if others manage your money vs investing the money into index funds.

There is also another large implication as a result of these calculations. If we know that the money can grow by a large amount, even with conservative expectations in long-term growth, then we shouldn’t fret over not being able to grow the “money fast enough”. For many, 7-10% growth per year sounds unexciting and even unreasonable. Why invest if we’re not going to go for the stars while doing so? The problem is that aiming for incredibly high returns is likely to increase the chance of risk as well.

If you look at the above table, there is an assumption that you could start out with $10 and take an 8% return for a comparatively small 80 cents that year. Sounds unexciting right?

Some may feel tempted to aim for much more in their returns. Let’s assume this person took a huge risk and as a result, they take a substantial loss, ranging from 10-50%. That would represent $5 (50% loss) to $9 (10% loss). Now this person will have to achieve incredibly high returns to even achieve the same 8% growth as the relatively conservative investor. This can become a losing cycle because to achieve such high returns in many cases would require high risk bets, which can cause further losses. To avoid such psychologically dire situations, it would have been better to start off relatively conservative from the beginning. Even one major loss after years of relatively strong growth can cause the investment portfolio to do worse than it should have.

If we know in the long-term there will be truly high gains (despite seemingly small returns in the short-term), it will be easier to feel peace of mind as we pursue our goals. It might seem boring to some but it is a better alternative to risky strategies that are unnecessary to achieve long-term goals that most pursue in their life such as retirement.

“Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it. ” – Albert Einstein

The famous Intelligent Investor book written by Columbia Professor Benjamin Graham was first published in 1949. Establishing the basis for what is now called value investing, this book set out a different way of thinking about stock market investing than what was prevalent in Wall Street at the time.

Even today, when most people think about stock market investing, their initial thoughts are line graphs about stock prices, daily percentage changes and people needlessly yelling on CNBC. This type of investing is technical analysis. Technical analysis on shares of AAPL (the ticker for the Apple company) means analyzing the trends of how the stock price has moved up within the last week, month, year, etc. But technical analysis says little about the quality of the actual company. Graham reminds us that when we are buying shares of a company, we are not merely buying a piece of paper that randomly goes up or down but we are buying actual ownership pieces of a live and functioning business. Buying a share of GOOGL means that over the long-term if Google does well, so will the stock.

While there are many lessons to potentially learn from reading this book, I present my 7 big takeaways from the book.

1. Differentiate present vs reality.

When a value investor buys a stock, they are not as interested in what the future of the company COULD be. They are more interested in knowing how the company is doing NOW and with slightly less importance, how it’s done in the past. An ‘intelligent investor’ would rather buy a company with a track record and currently favorable balance sheet than a company that has yet to prove itself and can bring you major losses. Graham emphasizes that there’s a very clear line between future speculation and present reality, and that we should keep a close eye on the current reality of any company.

2. Don’t believe that price has anything to do with quality.

If the price of a company is rising, it does not necessarily mean that the quality of the company is actually rising. Inversely, if the company’s stock price falls 20% within a day, it does not necessarily mean that the actual company has lost 20% of its total value within a day. Closely following the trends of the stock price movements to ascertain whether it’s a good company can be an easy way to misread the actual quality of the company. The market is irrational in the short-term and should not be seen as a guide for long-term investing. It is better to understand the meaning behind the company’s qualitative and quantitative position rather than its price position.

3. We really have no idea what is going to happen in the future.

To claim with certainty that a company will rise astronomically in the future or crash can be riddled with error. In truth, anything can happen. Graham, having grown up through multiple financial hardships and depressions was a firsthand witness to the realities of economic change. Because anything can happen, the best we can do is understand the position of the companies we have ownership of and spread our risk among multiple companies (otherwise known as diversification). Market timing can be dangerous.

4.”Getting good returns is easier than it looks but getting great returns is harder than it looks.”

This idea was shared in the context of ‘active’ vs ‘passive’ investing. As a passive investor, you buy a broad range of companies under the assumption that over the long-term the total economy as a whole will improve, meaning so will your financial position. But Graham states that if you try to beat the market, known as being an ‘active investor’, it’s going to take a lot of work. Graham also has a very interesting difference on how he sees risk. In finance academia, it is normally taught that to get more investment return, more risk needs to be taken on. Graham saw risk as a measure of how much work you did on researching your investments. From a value-investors perspective, it is possible to achieve higher investment return with lower risk.

5. Look beyond surface appearances and delve further.

Large public companies are fully aware and capable of manipulating how numbers will appear on earnings reports. Graham strongly urges reading company reports backwards, as management will hide everything they don’t want you to read near the end. Graham also recommends that investors conduct in-depth analysis by developing their own valuation of the company’s assets and stability of earnings rather than taking numbers at face value. By building your own independent thesis, you can catch issues or even opportunities that other investors might miss from just taking the numbers as is.

6. Always invest with a “margin of safety”.

‘Margin of safety’ is buying with a small to moderate ‘safety net’ on your investment. Even if negative results occur with your stock, you will ideally be protected by a strong book value or a strong business model or conservative assumptions on the company’s growth rates. Because stocks are being bought in such conservative ways, in the event of a market downfall, value investors would fare the best as they buy in such a price-conscious way.

7. Believe in yourself and your judgement, even if others hesitate or differ in tough market conditions.

Graham ends the book with an uplifting message reminding you to believe in yourself. Provided that you have your reasoning, data and experience to support your investing decisions, you should stick with your decision, even if the market is doing poorly in the short-term. The emotional fortitude to have differing opinions from others in times of stress, is incredibly important to succeed at investing in the long-term.

Overall, Graham presented a very lucid and rational perspective on investing, illustrating principles that still remains relevant many decades later. I utilize value investing principles like these for my own client’s portfolios.

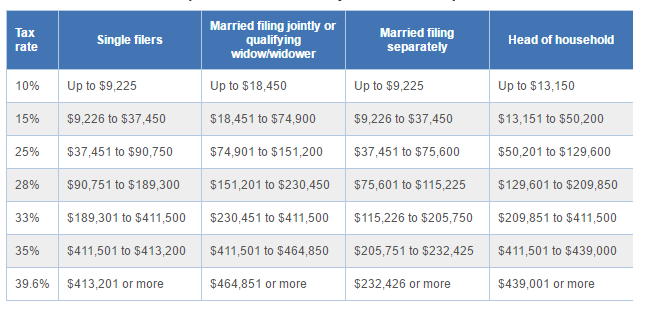

In America, we run on a ‘progressive tax’ system. This means that your tax rate will increase for each dollar that you are making. You won’t be taxed more on your “base amount” but you will be taxed extra for each additional dollar. Let’s say you are making $50k in wages a year for example. While each additional dollar you make will get taxed at 25%, parts of your original $50k will be taxed at 10% and 15%. The table below should explain this relatively well.

While you are in the lower income tax brackets, you won’t be taxed as much. But taxation can become a problem for you once you reach 28%, 33% and even 25% marginal tax. The solution in these cases would require special tax-advantaged strategies that help you avoid having atleast a quarter taken out of every dollar you make.

4 ways to avoid taxation on your investments.

Growth Stock Funds

Instead of putting money into stock funds or stocks that return hefty dividends, and therefore, cause taxation, you can invest in growth stock funds. Growth stocks don’t give dividends and instead reinvests the company’s profits back into the company in hopes of continued and higher growth. This means that the value of your fund can keep growing without you being taxed for a long time. You will usually only get taxed when you sell, triggering capital gain taxes. However, if you are very intentional about when you sell, you can save alot of money in the long-term. For example, selling growth stock funds in retirement when your taxable income will likely be much lower will potentially save you thousands of dollars in taxes.

Municipal Bond Funds

While bonds offer relatively high dividends, the taxation of those dividends is treated just like any other ordinary income. However, if you were to buy public state municipal bond funds, you would be able to get decent dividends while avoiding state and federal taxation. While these bonds can offer great cash flow for high-income earners, it is important to note how inflation may erode the long-term value of the income without a growth hedge.

IRA / 401k

A very common option for many people to save for retirement, putting money away into an IRA (individual retirement account) or a 401k (a type of defined contribution plan) can help save a sizable amount of money from tax. When you contribute to a traditional IRA or 401k, money is taken away from your paycheck before your money is subject to tax and placed into these retirement accounts. This removes sizable money from taxation. With a Roth IRA or 401k, the contributions are taxed immediately but you won’t be taxed on the growth later on. There are disadvantages with these accounts such as not being able to access the money till 59.5 in age or later. However, this can be a great option for most people who should be saving for retirement in the first place anyway.

Tax Loss Harvesting

This is a relatively advanced investing technique. I highly suggest staying away from this unless you really know what you’re doing or if you find a robo-advisor that does this for you. At TFP, our investing partner Betterment For Advisors allows tax loss harvesting for clients.

Tax Loss Harvesting works by selling a security that has suffered a loss, which triggers a capital gains loss. Having a capital gains loss can be a good thing because it offsets capital gains, meaning less taxable income. While you shouldn’t actively search for capital gains loss, being able to take advantage of opportunities when they arise can be profitable. Assuming you don’t collide with wash sales rules which would remove your capital gains loss benefit and assuming that you maintain your asset allocation, this can cause gains with substantial impact in the long run. You could potentially take up to $3000 per year in tax deductions from income with this type of strategy.

These are four ways to avoid taxation on investments.

Having a baby can change your life in many ways. But in the midst of it all, don’t forget these three important things you should be doing as a new parent.

#1: Get Life Insurance

If you don’t already have life insurance to cover your spouse, getting life insurance is now very important. Life insurance is protection against the risk that you die quicker than you should. If something should happen to you, your spouse and child would receive money that would ideally replace the income and services you brought to the house.

With life insurance, your family will not be in financial danger because of your lost income in the family. While you’re alive, life insurance gives you the confidence and peace of mind in your daily life to know that your loved one’s financial wellbeing would not change with you being gone. By failing to get life insurance, you put your spouse and child at risk.